Table of Contents

Points Miles and Bling (blog) contains referral or affiliate links. The blog receives a small commission at no additional cost to you. Thank you for your continued support. Credit Card issuers are not responsible for maintaining or monitoring the accuracy of information on this website. For full details, current product information, and Terms and Conditions, click the link included.

So it turns out the average number of credit cards Canadians hold is 2-3 per person. With that context in mind, it might be weird to read phrases like “XYZ card has a permanent spot in my wallet” and “I keep ABC card for the 5X earn rate and mobile device insurance”. After all, it sounds like the writer is holding on to certainly more than two credit cards. You would be right, and the natural question is, “Does applying for so many credit cards hurt your credit score?” Let’s unpack that in this article.

How Credit Scores Work

I know the PMB audience is financially savvy, so no need to spend too long discussing what is a “good” credit score. In Canada, a score of 660+ is considered good, and a score above 760 is considered excellent. With a credit score in this range, you should have no problems applying for a mortgage, car loan, or new credit cards.

Your credit score is made up of five categories, each with a different level of importance:

- 35% of score: on-time payment history

- 30% of score: credit utilization

- 15% of score: length of credit history / average age of accounts

- 10%: new credit applications

- 10%: credit diversification

Looking through the list, only 10% of your score comes from new credit card applications. The only other one affected is the average age of accounts, which drops if most of your credit cards are new. Even then, that accounts for only 25% of your credit score combined, so it’s much more important to focus on the others.

Essentially, pay all your credit cards on time (which you should be doing anyway, or this hobby is not for you), keep your credit utilization under 30% across your credit card folio, and maintain a number of keeper cards for the “average accounts of accounts” factor. Doing these three means 80% of your credit score is solid and the other 20% is not as impactful.

So… Applying for Cards Isn’t Bad?

Based on the above, applying for credit cards is only a small part of your score. However, new applications will typically incur a hard pull on your credit profile, which will decrease your score temporarily.

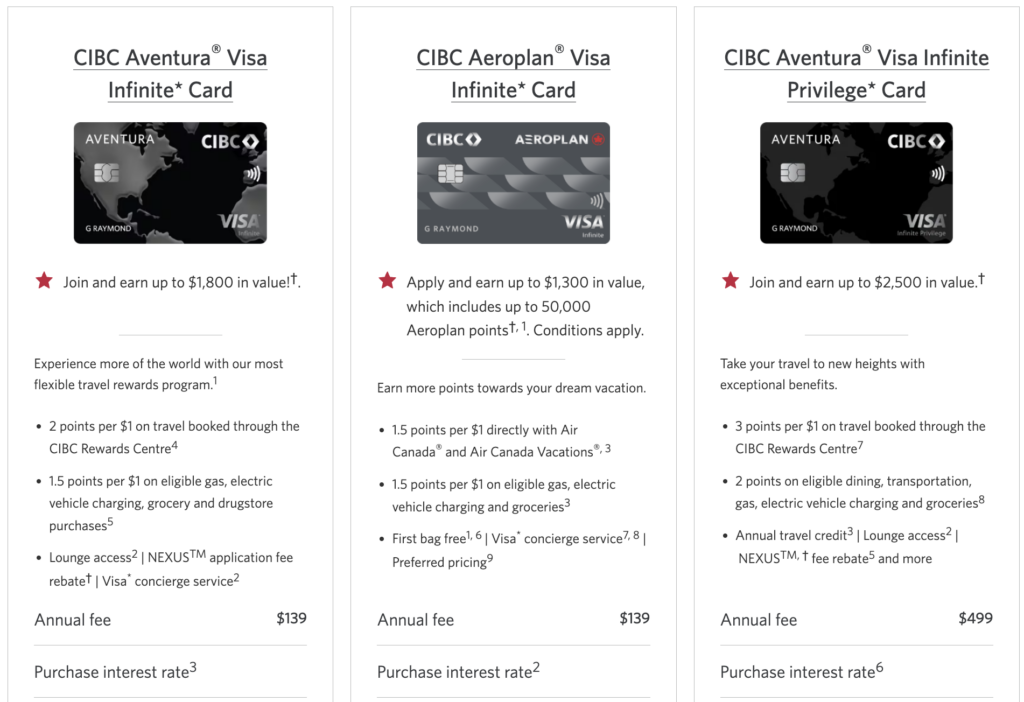

The keyword here is “temporarily”, because as time passes and you use your credit responsibly and pay it off consistently before your payment deadline, your score will recover quickly. There are ways to apply for cards and minimize the number of hard pulls, depending on the bank. For example, CIBC will use the same hard pull if applying for multiple cards within 90 days.

CIBC will reuse hard pulls within 90 days

To maintain a good length of credit history without paying annual fees, you can product switch some credit cards to a no annual fee version. Product switching stays on your credit profile as an existing credit line. For example, if you have a BMO eclipse Visa Infinite but find it no longer fits your lifestyle, you can product switch it to no-annual-fee BMO eclipse rise Visa Card and hold the latter indefinitely.

In fact, having multiple credit cards can even be good for “credit utilization” as you want to keep it to 30% or below. The more credit you have across your credit cards, the smaller percentage you’re utilizing on a regular basis (unless you spend more the more credit you have…).

Tracking Your Credit Score

It’s generally a good idea to keep a close eye on your credit profile to ensure accuracy and to ensure no one is stealing your identity. Furthermore, it’s a fast way to be alerted to late payments, such as if you set a recurring payment on a credit card you forgot about.

Some banks will let you check your credit for free through a direct link, which is the easiest way. You can also sign up with Credit Karma or Borrowell to see your score with TransUnion and Equifax, respectively. These are both free, while TransUnion and Equifax both charge a fee when going direct.

Takeaway

Applying for multiple credit cards doesn’t hurt your credit score as much as many people think. While new applications can cause a small, temporary dip, they only account for a minor portion of your overall score.

What really matters is paying your bills on time, keeping your credit utilization low, and maintaining a few long-term accounts. If you manage those well, holding multiple credit cards can be perfectly sustainable, even if applying for more cards than the Canadian average. 😉