Table of Contents

Points Miles and Bling (blog) contains referral or affiliate links. The blog receives a small commission at no additional cost to you. Thank you for your continued support. Credit Card issuers are not responsible for maintaining or monitoring the accuracy of information on this website. For full details, current product information, and Terms and Conditions, click the link included.

Travel insurance for award tickets can be a dicey topic, with so many “yikes” and “gotcha” possibilities. To be frank, that’s the case with insurance in general, but especially when you’re paying the base fare using points and the taxes and fees with a credit card.

There are basically two camps of people: those who do not ever pay attention to it and put the taxes onto whichever card they’re working on for minimum spend, or those who will carefully put every taxes and fees transaction on their “award travel insurance” card, even if they have to pay foreign transaction fees.

I was admittedly always in the first camp, but have migrated into the second, so let’s look at not just which cards cover you during irregular operations (IRROPS) on award travel, but why it’s worth the effort to use the right cards outside the obvious.

Emergency Medical Insurance

Before diving into the details, keep in mind that virtually every credit card that offers emergency medical insurance provides coverage simply because you’re a cardholder. Unlike many other travel insurance benefits, you do not need to charge any portion of your trip to the card to qualify.

Regular terms and conditions regarding factors like age and trip length still apply.

The One-Stop Solution

There are two credit cards in Canada that will cover you as long as you charge part of the trip to the card (i.e. taxes and fees), both issued by National Bank (foreign transactions incur a 2.5% fee):

- National Bank World Elite Mastercard

- National Bank Platinum Mastercard

As the names suggest, World Elite cards have better insurance coverage than Platinum cards, so that’s the one I’d recommend.

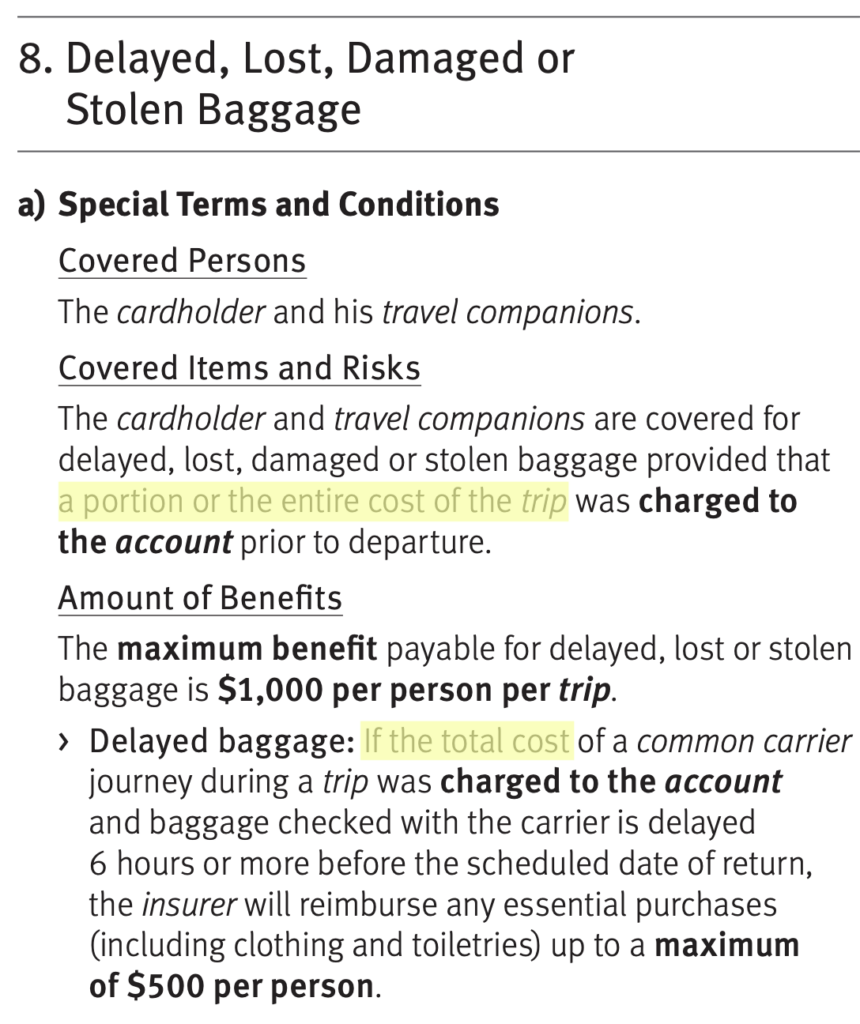

The main caveat is that the terms around delayed baggage are a little murky, as National Bank says, “The cardholder and travel companions are covered for delayed, lost, damaged or stolen baggage provided that a portion or the entire cost of the trip was charged to the account prior to departure.”

That should be crystal clear, except right underneath it, National Bank writes, “Delayed baggage: If the total cost of a common carrier journey during a trip was charged to the account.”

Conflicting T&Cs from National Bank

I know someone whose insurer initially denied a delayed baggage claim, but after he pointed the issue out to the underwriter, the insurer covered the claim in full.

Beyond “delayed, lost, damaged, or stolen baggage,” other benefits like trip cancellation, trip interruption, and flight delays should be covered without issue.

The National Bank World Elite Mastercard is also a great card for emergency medical insurance, with both age and trip-length limits on the extremely generous side. It covers up to $5,000,000 per person for out-of-province medical care, with the length of the trip covered dictated by age:

- Age 54 and under: 60 days

- Age 55 to 64: 31 days

- Age 65 to 75: 15 days

- Age 76 and over: no coverage

To qualify for this card’s rental car insurance, you must charge the entire cost of the rental to the card.

Many Cards Cover Award Travel, With a Caveat

While some credit cards cover all award bookings, others only cover award travel when you redeem the same rewards currency that the card earns. For example:

- The BMO Blue Rewards World Elite will cover trips booked with Blue Rewards points

- The TD Aeroplan Visa Infinite will cover trips booked with Aeroplan points

- The WestJet RBC World Elite will cover trips booked with WestJet points

- The RBC Avion Visa Infinite will cover trips booked with Avion points

- The Scotiabank Passport Visa Infinite will cover trips booked with Scene+ points

Charge your Aeroplan trip to an Aeroplan co-branded card for insurance coverage

Notably, the RBC British Airways Visa Infinite does not cover you for flights booked with British Airways Avios.

In all circumstances, you’ll also need to put all accompanying taxes and fees on that credit card to be eligible for insurance coverage.

Always Use the Credit Card With Insurance Coverage

For most of my life, I’d always put the taxes and fees on whatever card I was working on for minimum spend and never thought too much about the insurance. Every time I’d run into IRROPS, the airline covered additional shopping (for delayed baggage), hotel nights (for a delayed flight), and more.

I knew airlines don’t cover weather-related cancellations and that credit card insurance often proves most valuable in those situations. Frankly, I’ve been lucky enough to avoid them entirely so far.

My main reason for using the National Bank World Elite Mastercard (and continuing to pay the annual fee every year) for award bookings is simplicity. By charging every award booking to the same card, I ensure the card’s insurance applies to all of my trips, even if I never need to make a claim.

It also makes it much easier to track taxes, fees, refunds, and itinerary changes. More than once, I’ve received a refund on a cancelled card or forgotten which card I used for a particular booking. When I put every redemption on the same card, I can quickly track refunds and confirm they arrive as expected.

Put all your award taxes/fees on the same (insurance-provided) card for organizational purposes

Trust me, this is very important if you have multiple trips and multiple cards. The last thing you want is to cancel an award booking you made nearly a year ago and discover the refund will go back to a cancelled credit card (ask me how I know).

Takeaway

Award travel insurance is one of those things that’s easy to overlook until you actually need it. The National Bank World Elite Mastercard stands out because it covers most award bookings as long as you charge the taxes and fees to the card, eliminating many of the restrictions found on co-branded cards. Of course, to maximize points-earning, you can charge the taxes and fees to the co-branded credit card earning the currency you’re redeeming and still maintain insurance coverage.

Even if you never make a claim, know that putting every award booking on the same card creates a simple system for tracking insurance coverage, refunds, and change fees.